Powering Up Flexible Energy: Profit Engines for Utilities

As electrification outpaces grid expansion, Europe faces a looming capacity crunch. Decentralized flexibility from EVs to heat pumps offers the answer, with billions in value still unmonetized. This article outlines how utilities can unlock flex at scale and turn it into sustainable growth.

Europe may face a ~60 GW peak-capacity shortfall1 within the decade, with smart heat pumps and electric vehicles (EVs) scaling faster than the grid.

Demand-side flexibility of ~100 GW already exists, but less than 20% is monetized – meaning up to €58bn a year is being left on the table. Millions of smart, connected, schedulable “micro-assets” are waiting to be optimized:

- Electric vehicles often sit parked for ~23 hours a day, presenting ample opportunity to schedule charging times for off-peak, low-priced hours.

- Heat pumps can be scheduled to pre-heat homes ahead of the evening peak, and to manage output efficiently during high demand windows.

- Residential battery storage can be scheduled to arbitrage price volatility, and to deliver sub-second balancing and reserve support from behind the meter.

System-friendly heat pump operation has the potential to cut costs caused in the electricity system by 24%2 (compared to load-driven operation). Costs connected to electric vehicles can also be reduced by more than 70%2.

Flex is no longer just a “nice-to-have” for utility leaders, it is the next big chapter in the industry’s growth story. Rapidly monetizing flex at scale calls for a comprehensive blueprint that spans strategy, operating models, data, and security.

Succeeding in decentral flex trading requires an understanding of the market landscape and participants, the two key complimentary value pools, and how to build and execute a strategic transformation roadmap.

Market players and the flex shift

Flexibility has always been part of power systems. It initially came from central assets like thermal plants, hydropower, and pumped storage, which can ramp output and shift energy over time. TSOs and DSOs have long procured these services through established reserve and balancing mechanisms to ensure system stability.

What is changing is the source and scale of flexibility. As electrification and renewables accelerate, flexibility is increasingly coming from distributed, behind-the-meter assets - EVs, heat pumps, and residential batteries.

According to projections for the German market, the annual flexibility energy potential is expected to almost double by 2030, increasing from around 16 TWh today to approximately 31 TWh.

The strongest growth is anticipated from EVs (from ~2.7 to 8.2 TWh), heat pumps (from ~3.3 to 11.7 TWh), and residential batteries (from ~1.3 to 2.9 TWh). Aggregated as fleets, these assets can respond rapidly and help manage volatility, local grid constraints, and peak load.

Importantly, these new flexibility sources can be unlocked in two distinct ways:

- Implicit flexibility occurs when customers adjust their consumption in response to dynamic price signals, without any direct control or formal activation by a utility or aggregator.

- Explicit flexibility, by contrast, is marketized and contractually secured: customers opt in, devices are remotely controlled, and flexibility is measured, verified, and traded across system and energy markets.

This shift is driving new players to enter the market and compete for customer access, device integration, and control. For utilities, decentralized flexibility is therefore becoming both a critical grid lever and a commercial opportunity.

Those that strategically combine implicit and explicit flexibility across their portfolios can differentiate tariffs, reduce churn, and unlock meaningful P&L impact at scale. This article focuses on how to make decentralized flexibility work - and how to turn it into sustainable profit.

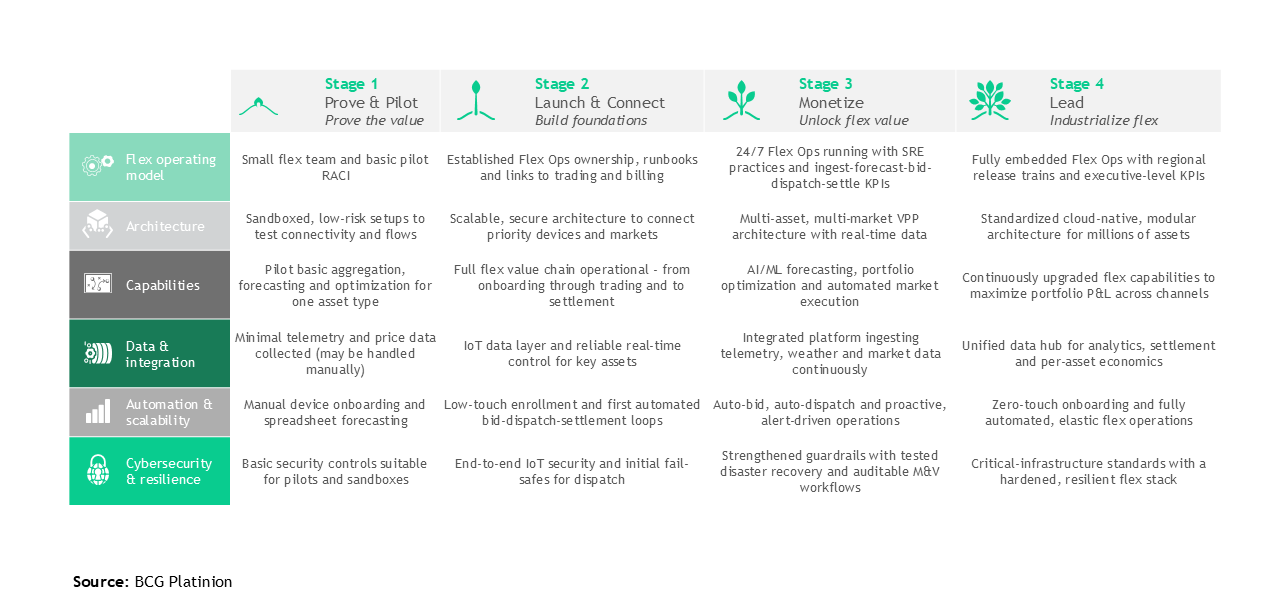

The top 6 flex readiness factors

In our experience, six main dimensions separate pilots from profitable scale. Utility leaders need to gain a holistic view across these dimensions, identify gaps, and work towards maturity in each:

- Operating model – 24/7 Flex Ops, SRE practices, model governance, and product ownership are crucial factors. These operating model features take a utility provider from being a planner to a dynamic, real-time system operator.

- Capabilities – All flex-relevant capabilities need to be covered in a single value chain, including aggregation, forecasting, optimization, and market execution. AI and ML-driven forecasting and optimization of available flexibility will be competitive differentiators, providing the necessary intelligence to operate in real-time.

- Architecture – Connecting a wide range of devices, scaling to millions of assets, and interfacing securely with markets and distribution system operators (DSOs) is essential. Flexibility only creates value if it can be delivered reliably, at scale, and in the right place at the right time.

- Scalability and automation – The fundamentals include low-touch device onboarding, automated bid-dispatch-settlement loops, and cloud-native elasticity. Low-touch onboarding cuts costs per device and improves flex revenue, while automation takes efficiency to the next level with self-service enrolment and standardized asset qualification.

- Security and resilience – Implement end-to-end IoT security, fail-safes, disaster recovery measures, and standards compliance. All communications need to be protected with sophisticated encryption and authentication to prevent unauthorized access and manipulation of energy flows.

- Data and integration – A layer needs to be implemented to manage IoT connectivity and link distributed assets (smart appliances, home batteries, EV chargers) to your control platform in real-time. Control signals from IoT cloud APIs, smart meters, and HEMS need to be received and translated into dispatch commands in an interoperable way.

Utility players must move from manual device onboarding, spreadsheet-based forecasting, and manual trade execution to fully automated, end-to-end flexibility trading workflows. These must be designed to scale across large asset portfolios and handle six-digit trade volumes per day.

The journey towards readiness is made up of four stages, which can serve as a due-diligence framework.

.png)

European incumbents have to act now on flexible energy, with household flex presenting an opportunity to close system peaks and tap into this €58 billion a year opportunity. Germany is among the fastest moving markets, with providers positioning themselves to navigate mounting volatility,address capacity gaps, and respond to growing bill pressure from customers.

A four-step roadmap to get started:

- Step 1 – Establish ambition and baseline maturity. Define your target MW to revenue goals, your key segments, and run a maturity assessment across the six readiness dimensions outlined above.

- Step 2 – Build, partner, or buy to close capability gaps. It is advisable to build in instances that call for differentiation or IP, partner to accelerate progress in problem areas, and buy when it comes to commodity components like adaptors.

- Step 3 – Launch a pilot, then scale to overcome plateaus. Start with a single asset type and specific approach (such as EVs with dynamic tariffs and aggregation). Prove the pilot end-to-end, from onboarding to billing, then add heat pumps, batteries, new channels, and regions to plateau upwards.

- Step 4 – Industrialise operations. Set up flex ops with 24/7 coverage, model governance, release trains that respect regional certifications, and KPIs that executives can steer. KPI examples include the success rate of onboarding, event delivery percentages, €/MWh flexibility, and billing accuracy.

At BCG Platinion, we help our clients to achieve discipline and close the ingest, dispatch, ETRM, capture, back-allocation loop, equipping models to pay out and prevent disputes eating into margins. Remember to design for scale, and that progressively overcoming plateaus beats big bets.

At BCG Platinion, we support clients in building exactly these capabilities. In our next article, we will take a closer look at the six readiness factors that matter most.

1. https://capital-riesgo.es/en/articles/opportunities-for-market-players-along-the-residential-energy-flexibility-value-chain/

2. https://neon.energy/Neon-Mehrwert-Flex-EN.pdf